Navigating the world of health insurance can be complex and daunting, but understanding its fundamental aspects can significantly ease the process. This comprehensive guide will break down what health insurance is, why it’s essential, how it works, the different types of health insurance plans, and tips for choosing the right policy for you and your family.

What is Health Insurance?

Health insurance is a type of coverage that pays for medical and surgical expenses incurred by the insured. It can also cover the costs of preventive care, prescription drugs, and mental health services. Health insurance can be purchased individually, provided through an employer, or obtained through government programs.

Why Health Insurance is Essential

- Financial Protection: Health insurance helps protect you from high medical costs. Without insurance, an unexpected illness or accident could lead to financial ruin.

- Access to Care: Having health insurance ensures that you have access to necessary medical services when you need them, including regular check-ups, emergency services, and specialist care.

- Preventive Services: Many health insurance plans cover preventive services such as vaccinations, screenings, and wellness check-ups, which can help detect and treat health issues early.

- Legal Requirement: In some regions, having health insurance is mandatory. For example, the Affordable Care Act (ACA) in the United States requires most individuals to have health insurance or pay a penalty.

How Health Insurance Works

Health insurance operates on the principle of risk pooling, where policyholders pay premiums into a collective fund managed by the insurance company. When a policyholder needs medical care, the insurance company pays for the covered services according to the policy terms. Here’s a closer look at how health insurance works:

- Premiums: These are regular payments made to the insurance company to keep the policy active. Premiums can be paid monthly, quarterly, or annually.

- Deductibles: This is the amount you pay out-of-pocket for healthcare services before your insurance starts to pay. Higher deductibles usually result in lower premiums.

- Copayments and Coinsurance: After meeting your deductible, you may be required to pay a copayment (a fixed amount) or coinsurance (a percentage of the cost) for medical services.

- Out-of-Pocket Maximum: This is the maximum amount you will pay for covered services in a policy period, typically a year. After reaching this limit, the insurance company pays 100% of covered costs.

Types of Health Insurance Plans

There are several types of health insurance plans, each with its own structure and benefits. Understanding these plans can help you choose the one that best fits your needs.

- Health Maintenance Organization (HMO):

- Requires you to choose a primary care physician (PCP).

- Needs referrals from your PCP to see specialists.

- Provides coverage only within a network of approved providers.

- Typically has lower premiums and out-of-pocket costs.

- Preferred Provider Organization (PPO):

- Offers more flexibility in choosing healthcare providers.

- Does not require referrals to see specialists.

- Covers out-of-network care, but at a higher cost.

- Higher premiums and out-of-pocket costs compared to HMOs.

- Exclusive Provider Organization (EPO):

- Combines elements of HMOs and PPOs.

- Requires you to use a network of providers, except in emergencies.

- Does not require referrals for specialists.

- Lower premiums than PPOs but limited provider options.

- Point of Service (POS):

- Requires a primary care physician and referrals for specialists.

- Offers some out-of-network coverage but at higher costs.

- Balances the cost-saving features of HMOs with the flexibility of PPOs.

- High-Deductible Health Plan (HDHP) with Health Savings Account (HSA):

- Features higher deductibles and lower premiums.

- Eligible for an HSA, which allows you to save pre-tax money for medical expenses.

- Ideal for healthy individuals who don’t expect frequent medical expenses.

Government-Sponsored Health Insurance Programs

In addition to private insurance plans, several government-sponsored programs provide health coverage, especially for specific groups such as low-income individuals, the elderly, and veterans.

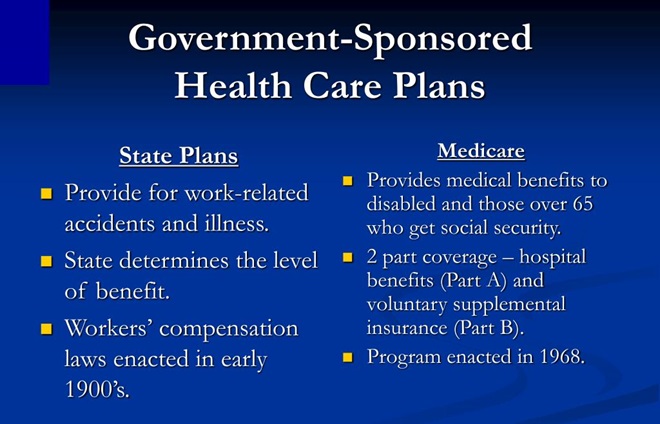

- Medicare: A federal program for people aged 65 and older, and some younger individuals with disabilities. It includes Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage).

- Medicaid: A joint federal and state program providing health coverage for low-income individuals and families. Eligibility and benefits vary by state.

- Children’s Health Insurance Program (CHIP): Provides low-cost health coverage to children in families that earn too much to qualify for Medicaid but cannot afford private insurance.

- Veterans Health Administration (VHA): Offers healthcare services to eligible veterans at VHA facilities.

Choosing the Right Health Insurance Plan

Selecting the right health insurance plan requires careful consideration of your healthcare needs and financial situation. Here are some tips to help you make an informed decision:

- Assess Your Needs: Consider your health status, frequency of doctor visits, prescription medications, and whether you need specialist care.

- Budget Considerations: Evaluate your ability to pay premiums, deductibles, copayments, and coinsurance. Choose a plan that balances cost and coverage.

- Provider Network: Ensure your preferred doctors, hospitals, and specialists are in the plan’s network.

- Coverage Options: Review the covered services, including preventive care, prescription drugs, mental health services, and any other specific needs.

- Plan Flexibility: Consider whether you need a plan that offers flexibility in choosing healthcare providers and the necessity of referrals.

Conclusion

Understanding health insurance is crucial for making informed decisions about your healthcare coverage. By grasping the basics of how insurance works, the different types of plans available, and the importance of coverage, you can select a plan that best suits your needs and provides financial protection against unexpected medical expenses. With the right health insurance, you can ensure access to quality healthcare while maintaining financial stability.