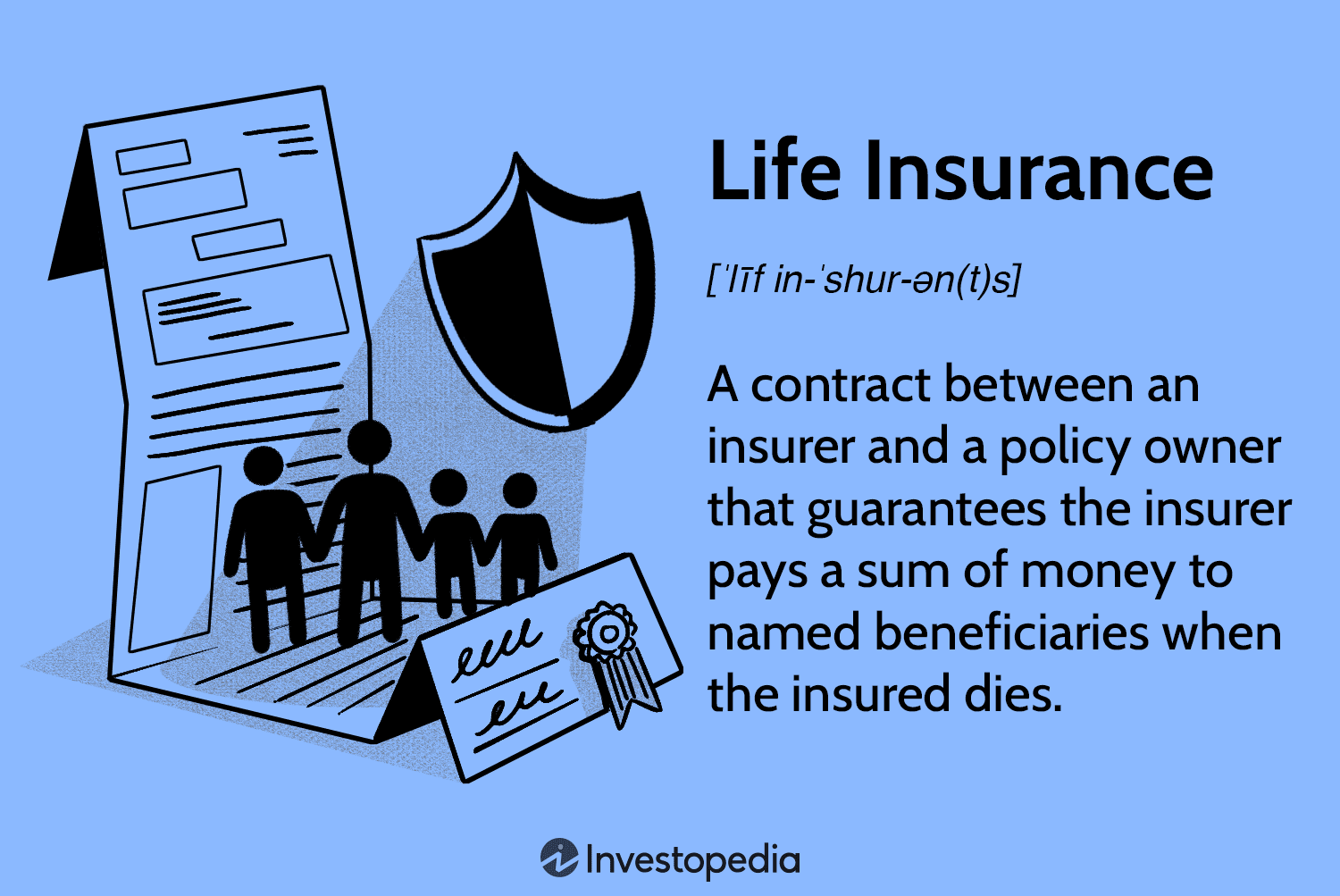

An insurance provider and you sign a contract for life insurance coverage. The insurer receives a death benefit in exchange for regular payments, or premiums. This money is paid to the beneficiaries of your life insurance policy, who are usually your spouse, children, or other family members.

Who Needs life Insurance Coverage?

Having life insurance coverage could be an essential safety net if you are the person who provides all of the care for others. For example, if you are the major provider, a parent, a homeowner, or you have co-signed debt, you may need life insurance. The money can be used for anything by the recipients, such as clearing debts, making up for missed income, or covering burial and funeral costs.

How to buy a life insurance policy

You have the following options if you’re trying to get a life insurance policy:

- online. Depending on the type of coverage you select, you may be able to apply online, buy a policy, and have coverage the same day. This is known as instantaneous life insurance. In order to determine your rate, many insurance companies and brokerages ask a series of questions about your health and lifestyle in addition to using algorithms to determine your eligibility for coverage.

- via an agent or broker. In the event that you are a high-risk applicant or just require assistance with the application process, contact a life insurance agent or broker. Captive agents sell policies from a single company, such as State Farm, whereas independent agents typically supply policies from multiple firms.

- directly from the insurance provider. Most insurance companies allow you to buy a policy online, over the phone, or in person. Before choosing a carrier, be sure you’re getting the best coverage at the best price by comparing quotes.

Which life insurance plan is best for me?

The two main types of life insurance are usually term and permanent. You will only be covered by a term life policy for a set period of time, such as 10 or twenty years. Permanent life insurance can protect you for the remainder of your life and typically includes a cash value component.

What’s the right amount to spend on life insurance?

When calculating how much life insurance you need, take into account your present as well as your future financial obligations. Try to find a policy that fits them after that.

As an example:

- Add up all long-term debts, such mortgages or college tuition.

- To make sure your dependents are covered when you pass away, multiply your annual income by the number of years you would like coverage for.

- Any amount that can be used to cover these expenses should be subtracted from your current assets or income.

How much does a life insurance coverage cost?

Generally speaking, term life insurance is less expensive than permanent life insurance. When comparing the various types of permanent coverage, whole life is typically more expensive than universal life. Finding a policy that is inexpensive is essential.

If you don’t make payments, the insurance may cancel your coverage, leaving your beneficiaries underpaid. Before making a purchase, it’s a good idea to compare life insurance quotes from several providers because costs might vary significantly throughout insurers.

Compare the top companies offering life insurance.

Once you’ve decided on the type of policy and amount of coverage you need, it’s important to select the finest life insurance company. Check out our reviews of life insurance to find out about some of the top companies on our list.

Obtain the best possible life insurance coverage.

Are you looking for the best life insurance coverage for a specific reason? Check out our roundups on:

- leading suppliers of term life insurance.

- leading suppliers of whole life insurance.

- Leading providers of burial life insurance.

- best-rated life insurance for seniors.

- Leading instant life insurance companies.

- greatest life insurance that requires no medical examination.

- Best life insurance with a premium refund.

- best child life insurance coverage.

- The greatest protection against unintentional death and dismemberment.

Interpreting life insurance quotes

A life insurance quotation is only an estimate that tells you how much the policy will cost. A few factors, like the type of insurance you’re looking for, the amount of coverage you need, and personal details like your age and smoking history, all influence quotes.

How to assess life insurance quotations

It’s a good idea to compare life insurance quotes from various providers before to buying a policy. But when you do, make sure to assess the same features that every company has to offer. For example, select the same kind of policy, the same amount of coverage, the same term length, and the same personal details for each quote. This will help you get a more accurate comparison.

Quotes and rates related to life insurance

- An estimate of the price based on the least amount of information available is called a quote.

- Rates reflect the true cost of the insurance.

- When you apply for a policy, the insurer typically obtains more detailed information about you, which may result in a difference in your final price from the quotation that was initially provided.

- This is your ultimate rate or premium.

- Your life expectancy is typically used as the foundation for life insurance rates.

- Every life insurance provider bases their estimate of your life expectancy on a number of variables, such as your health, lifestyle, driving history, and family medical history.

Techniques used to rate life insurance

NerdWallet evaluates life insurance policies based on three primary criteria: weighted averages of financial strength ratings, which indicate a company’s ability to pay future claims; individual life insurance complaint index scores; and customer experience. We include account website transparency and communication ease in the area of customer experience, which looks at the amount of online policy information. The data were translated into a curved 5-point scale, which we used to calculate each insurer’s rating. Although these rankings are meant to be used as a guide, we highly suggest you to shop about and compare insurance quotes from other providers in order to obtain the best available rate. NerdWallet does not offer compensation for reviews. Examine our editorial guidelines.

Techniques for Filing Insurance Appeals

NerdWallet looked at reports that state insurance regulators had received and sent to the National Association of Insurance Commissioners in 2020–2022. Every year, the NAIC compiles a complaint index for each subsidiary, comparing the percentage of complaints to the size of the business or the percentage of total premiums in the sector to assess how insurers compare to one another. To evaluate a company’s complaint history, NerdWallet developed a similar index that is weighted by the market shares of each subsidiary and is established for each insurer over a period of three years. NerdWallet does independent data analysis and draws its own conclusions without consulting the NAIC. The ratios for cars, housing (including renters and condos), and life insurance are all different.

What amount of life insurance is required?

Your current and future financial needs will dictate the amount of life insurance you require. When figuring out the right amount of coverage, consider all of your current and future financial obligations, including income, bills, and daily spending.

What is the average premium for life insurance?

According to Quotacy, the average monthly premium for life insurance is $26. The foundation for this pricing is a $500,000, 20-year term life insurance policy for a healthy 40-year-old individual. Monthly premiums for a full life coverage worth $500k typically come to $540.

Which are the main types of coverage for life insurance?

The two main types of insurance are term and permanent life insurance. Term life has a limited duration and is fleeting. Permanent life insurance policies often last the duration of your life and build up cash value over time.

Do I have to go through a medical examination?

For some life insurance policies, a medical examination might be required. These tests give insurers a more precise picture of your general health and, by extension, your life expectancy. The insurance company uses the results to determine your coverage eligibility and rate. If you would want to skip the exam, take into account not having life insurance for medical exams. But because the insurer is unable to calculate your life expectancy precisely, the costs for various types of insurance may be greater.

How should I compare life insurance companies?

It’s critical to consider a life insurance company’s complaint history and financial soundness while assessing them.

Institutions like AMhighest rate of financial stability. They often display the likelihood that an insurer will pay out on a future claim. Generally speaking, NerdWallet suggests comparing life insurance companies with an A- or higher rating.

The complaint statistics from the National Association of Insurance Commissioners may assist paint a clearer picture of how well a company serves its clients. According to NerdWallet’s life insurance rating algorithm, businesses with fewer state regulator complaints are given preference.